What Does Medicare Not Cover: Key Gaps Explained

Medicare is a vital health insurance program for millions of Americans aged 65 and older as well as younger individuals with qualifying disabilities. However, many beneficiaries are surprised to discover that Original Medicare (Part A and Part B) does not cover everything. Understanding what is excluded can help you avoid unexpected medical bills and plan for additional coverage. This article explains the most significant gaps in Medicare coverage so you can make informed decisions about your health and finances.

Original Medicare was designed to cover hospital stays, doctor visits, and some preventive services, but it leaves many essential services and items uncovered. Without supplemental coverage, you could face high out-of-pocket costs for services like dental care, vision exams, hearing aids, and long-term care. By learning what Medicare does not cover, you can explore options such as Medicare Advantage plans (Part C) or Medigap policies to fill these gaps. Below we break down the major exclusions and offer practical advice for protecting your health and wallet.

Dental Care: A Major Gap in Medicare Coverage

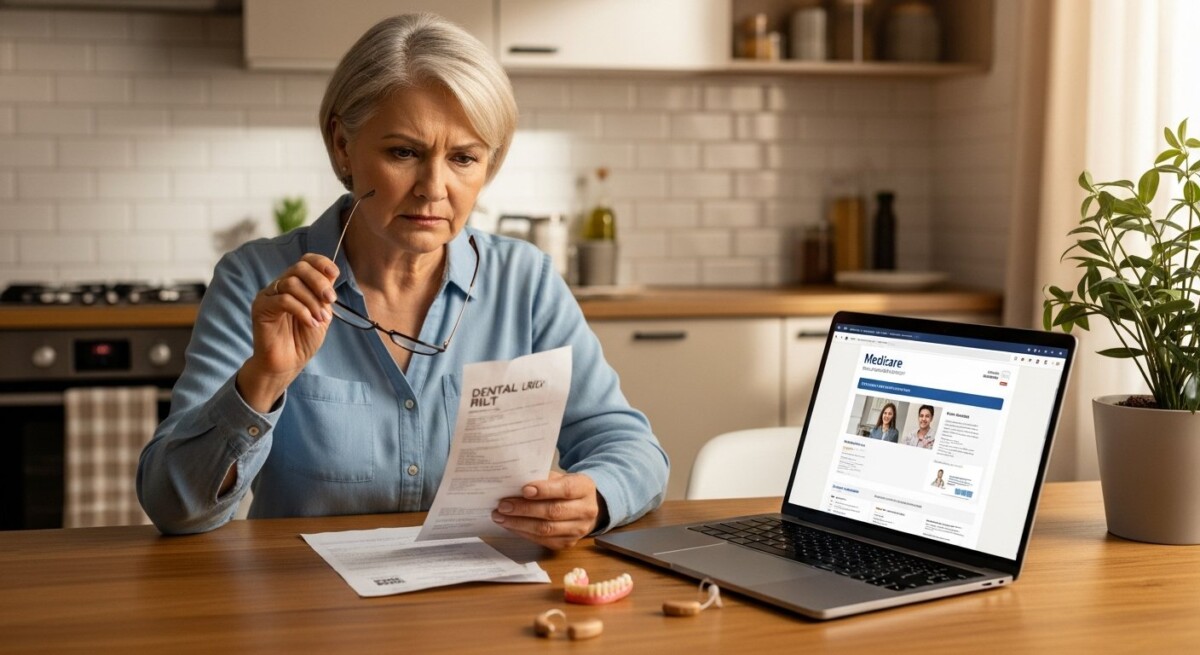

Original Medicare does not cover routine dental care, including cleanings, fillings, extractions, dentures, or dental exams. This exclusion surprises many beneficiaries who assume their health insurance includes basic dental services. Medicare Part A may cover dental procedures if they are performed during a covered hospital stay, such as an emergency tooth extraction before a heart surgery, but this is rare and limited.

For routine dental care, you will need to pay out-of-pocket or purchase a separate dental insurance plan. Some Medicare Advantage plans include dental benefits, but coverage levels vary widely. If you need dentures or complex dental work, the costs can quickly add up. In fact, a single dental implant can cost thousands of dollars. Planning ahead for dental expenses is critical because Medicare does not provide any routine dental coverage at all.

To manage these costs, consider enrolling in a standalone dental insurance policy or a Medicare Advantage plan with robust dental benefits. You can also use dental discount programs or negotiate cash rates with your dentist. The key is to understand that Medicare will not pay for your annual cleaning or a new set of dentures, so you must budget accordingly.

Vision and Hearing: Routine Exams and Devices Are Not Covered

Original Medicare does not cover routine vision exams, eyeglasses, or contact lenses. It only covers eye exams related to medical conditions such as diabetic retinopathy, glaucoma, or macular degeneration. Similarly, Medicare Part B covers cataract surgery and one pair of corrective lenses after surgery, but it does not pay for routine vision tests or glasses for general vision correction.

Hearing care is another area with limited coverage. Medicare Part B covers diagnostic hearing tests if ordered by a physician to evaluate a medical condition, but it does not cover routine hearing exams, hearing aids, or fittings for hearing aids. These devices can cost between $1,000 and $6,000 per ear, and most beneficiaries must pay the full price themselves.

If you need vision or hearing assistance, explore Medicare Advantage plans that include these benefits. Many Advantage plans offer allowances for eyeglasses, contact lenses, and hearing aids. Alternatively, you can purchase standalone vision and hearing insurance or use discount programs. Without supplemental coverage, you will bear the full cost of these essential services.

Long-Term Care: Medicare Does Not Pay for Custodial Care

One of the most significant gaps in Medicare is long-term care. Medicare provides limited coverage for skilled nursing facility care after a hospital stay, but it does not cover custodial care, which is help with daily activities like bathing, dressing, eating, and using the bathroom. Custodial care accounts for the majority of long-term care services and is often provided in nursing homes, assisted living facilities, or at home by home health aides.

Medicare Part A covers up to 100 days of skilled nursing facility care per benefit period, but only if you meet strict conditions: you must have a qualifying hospital stay of at least three days, need skilled nursing or therapy services daily, and be admitted to a Medicare-certified facility within 30 days of leaving the hospital. After day 20, you pay a daily coinsurance amount. Once you no longer need skilled care, Medicare stops paying entirely.

For long-term custodial care, you must rely on other resources such as Medicaid (if you meet income and asset limits), long-term care insurance, or personal savings. Planning for long-term care is essential because the costs can deplete retirement funds quickly. In our guide on understanding hospital bill coverage, we explain how Medicare’s limited coverage for extended stays can leave you with large bills if you need long-term care.

Prescription Drugs: Part D Is Not Part of Original Medicare

Original Medicare (Parts A and B) does not cover most prescription drugs you take at home. This is a critical gap that many beneficiaries discover only after they need a costly medication. To get prescription drug coverage, you must enroll in a separate Medicare Part D plan or choose a Medicare Advantage plan that includes drug coverage (MAPD).

Part D plans have formularies that list covered drugs, and they may place medications in tiers with different copayments or coinsurance. Some drugs may require prior authorization or step therapy. If you do not enroll in Part D when you are first eligible and later decide you need it, you may face a late enrollment penalty that increases your premium permanently.

It is important to review Part D plans annually during the Open Enrollment Period (October 15 to December 7) because formularies and costs change each year. If you take expensive medications, consider a plan that covers them at a lower tier. Without drug coverage, a single prescription could cost hundreds of dollars per month.

Medical Equipment and Supplies: Not All Items Are Covered

Medicare Part B covers durable medical equipment (DME) such as wheelchairs, walkers, hospital beds, and oxygen equipment, but only if it is medically necessary and prescribed by a Medicare-enrolled provider. However, Medicare does not cover all types of equipment or supplies. For example, it generally does not cover:

- Items for comfort or convenience, such as grab bars for the bathroom or air conditioners.

- Hearing aids and related supplies (as mentioned above).

- Most over-the-counter medications and supplies.

- Orthopedic shoes or shoe inserts unless they are part of a leg brace.

Even when Medicare covers DME, you typically pay 20 percent of the Medicare-approved amount after meeting your Part B deductible. Some equipment must be rented rather than purchased, and you may need to use a Medicare-approved supplier. If you need specialized equipment, check with your doctor and supplier to confirm coverage before buying.

For more details on what is covered, see our article on 24-hour in-home hospice care benefits, which explains coverage for end-of-life equipment and services.

Alternative Medicine and Wellness Services

Medicare does not cover most alternative or complementary therapies, including acupuncture (with limited exceptions for chronic low back pain), chiropractic services (except for manual manipulation of the spine to correct a subluxation), massage therapy, naturopathy, and most nutritional counseling. These services are popular for managing pain and stress, but beneficiaries must pay for them out-of-pocket unless they have supplemental coverage.

Some Medicare Advantage plans offer wellness benefits such as gym memberships, acupuncture, or chiropractic visits. If these services are important to you, compare Advantage plans carefully during enrollment. Original Medicare also covers some preventive services like cardiovascular screenings and obesity counseling, but the range of wellness services is narrow compared to private insurance plans.

Cosmetic Surgery and Elective Procedures

Medicare does not cover cosmetic surgery or procedures performed solely to improve appearance. This includes facelifts, breast augmentation, liposuction, and similar elective surgeries. However, Medicare may cover reconstructive surgery if it is needed to improve the function of a body part or to correct a deformity resulting from injury, illness, or congenital defect. For example, breast reconstruction after a mastectomy is covered.

If you are considering any elective procedure, confirm with your provider that Medicare will not deny coverage. You may need to pay the entire cost upfront or seek financing options. Always get a written statement from Medicare or your plan before proceeding with surgery to avoid surprise bills.

Travel and Emergency Care Outside the United States

Original Medicare generally does not cover health care services you receive outside the United States and its territories. There are very limited exceptions, such as when you are in a foreign hospital that is closer to your U.S. residence than the nearest U.S. hospital, or during a medical emergency on a cruise ship within U.S. territorial waters. In most cases, you will be responsible for 100 percent of the costs of foreign medical care.

If you travel frequently or live abroad part of the year, consider purchasing a Medigap plan that offers foreign travel emergency coverage. Most Medigap plans (C, D, F, G, M, and N) cover 80 percent of emergency care costs outside the U.S. after you meet a $250 annual deductible, up to a lifetime maximum of $50,000. Medicare Advantage plans rarely cover foreign care, so check your plan details before traveling.

Frequently Asked Questions

Does Medicare cover dental implants?

No, Original Medicare does not cover dental implants or any routine dental procedures. Some Medicare Advantage plans may offer limited dental benefits, but implants are often excluded or have high out-of-pocket costs.

Does Medicare cover hearing aids?

Original Medicare does not cover hearing aids or exams for fitting them. You can purchase a Medicare Advantage plan with hearing benefits or buy a standalone hearing insurance policy.

Does Medicare cover long-term care in a nursing home?

Medicare covers only skilled nursing facility care for a limited time (up to 100 days per benefit period) and only if you meet strict requirements. Custodial care in a nursing home or assisted living is not covered.

Can I get coverage for alternative medicine through Medicare?

Original Medicare covers very few alternative therapies. Acupuncture is covered only for chronic low back pain, and chiropractic is limited to spinal manipulation. Some Medicare Advantage plans offer additional wellness benefits.

How to Fill the Gaps in Medicare Coverage

Understanding what Medicare does not cover is the first step to protecting yourself from high medical costs. The most common solution is to enroll in a Medicare Advantage plan (Part C), which combines Parts A and B and often includes additional benefits like dental, vision, hearing, and prescription drugs. Alternatively, you can keep Original Medicare and add a Medigap policy to cover coinsurance, copayments, and deductibles, along with a Part D plan for medications.

Each option has trade-offs. Medicare Advantage plans typically have lower premiums but restrict you to a network of providers. Medigap plans offer more flexibility to see any Medicare-accepting provider but have higher premiums. To choose the best path for your needs, compare plans based on your health conditions, preferred doctors, and budget. For a deeper look at how costs change over time, read our analysis on whether Medicare costs go up every year.

You should also review your coverage annually during the Medicare Open Enrollment Period. Plans change their benefits, costs, and networks each year, so what worked last year may not be the best option today. If you have specific health needs such as cancer treatment or chronic conditions, check whether your plan covers the specialists and medications you require. Our guide on 3D mammogram coverage shows how preventive services can vary by plan.

Finally, remember that no single plan covers everything. Even with comprehensive Medicare Advantage or Medigap coverage, you may still have out-of-pocket costs for services like dental implants, hearing aids, or long-term care. Budgeting for these expenses and exploring supplemental insurance or discount programs can help you manage your overall healthcare costs.

Knowing what Medicare does not cover empowers you to make proactive decisions about your health coverage. Whether you choose Original Medicare with supplemental plans or a Medicare Advantage plan, the key is to understand your policy and plan for the gaps. If you need personalized assistance, licensed insurance agents can help you compare options in your area. For more information on hospital coverage specifics, see our complete guide on whether Medicare covers 100 percent of hospital bills.