How to Avoid Medicare Fraud and Abuse: Key Steps

Medicare fraud and abuse cost taxpayers billions each year and put beneficiaries at risk of identity theft, incorrect medical records, and financial loss. Scammers constantly develop new tactics to steal your Medicare number or bill the program for services you never received. Understanding how to avoid Medicare fraud and abuse is essential for protecting your benefits and your personal information. By staying vigilant and following a few simple practices, you can safeguard your coverage and help keep the system honest for everyone.

Recognizing Common Medicare Fraud Schemes

Fraudsters often target older adults and people with disabilities because they hold Medicare cards and may be less familiar with scam techniques. One of the most common schemes involves a caller who pretends to be from Medicare and asks for your Medicare ID number or bank account details. Medicare will never call you to sell plans, ask for payment over the phone, or request your Social Security number unless you have initiated contact. Another frequent fraud is equipment billing: a company sends you a back brace or a walker you did not order, then bills Medicare for it. If you accept the item, your records show you received it, and Medicare may deny future legitimate claims for similar equipment.

Phantom billing is equally dangerous: a provider submits claims for appointments or procedures you never had. You might notice this on your Medicare Summary Notice (MSN) or Explanation of Benefits (EOB). Identity theft also occurs when a scammer uses your Medicare number to receive medical care or prescription drugs, which can lead to incorrect diagnoses on your record. In our guide on Stop Medicare Fraud: Essential Tips to Safeguard Your Benefits, we explain how these schemes operate and what red flags to watch for.

Protecting Your Medicare Card and Number

Your Medicare card contains your Medicare Beneficiary Identifier (MBI), which is a unique number that should be treated like a credit card number. Never share your MBI with anyone who contacts you unsolicited. Carry your card only when you need it for a medical appointment, and keep it in a safe place at home otherwise. If you lose your card, report it immediately to the Social Security Administration (SSA) and request a replacement. You can also log into your mySocial Security account to print a temporary card.

Be cautious about giving your Medicare number over the phone or through email. Legitimate healthcare providers will already have your information on file if they are in-network. If someone claiming to be a pharmacy, equipment supplier, or insurance agent asks for your number to verify coverage, hang up and call Medicare directly at 1-800-MEDICARE to confirm the request. Remember that Medicare will never call you to sell plans or ask for payment. For more details on reporting suspicious activity, see our article on How to Report Medicare Fraud: Essential Steps to Safeguard Your Rights.

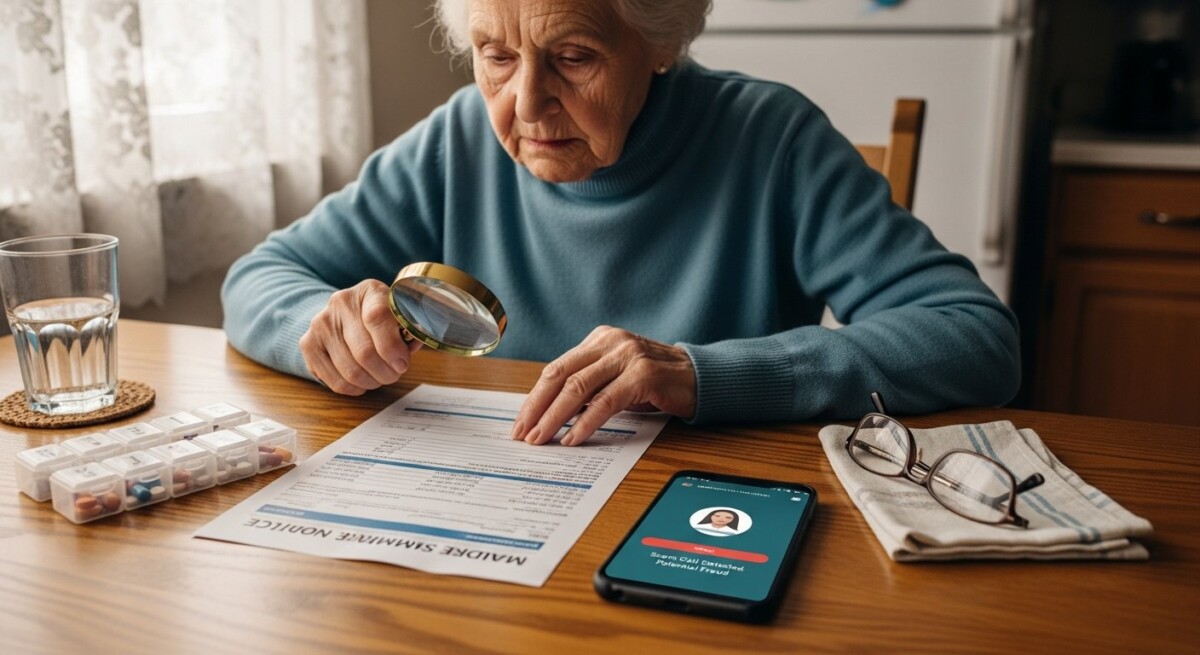

Reviewing Your Medicare Summary Notices and EOBs

One of the most effective ways to detect fraud early is to carefully review every Medicare Summary Notice (MSN) you receive. The MSN is a quarterly statement from Medicare that lists all services billed in your name. Check each line for services, equipment, or supplies you did not receive. Also review your Explanation of Benefits from your Medicare Advantage plan or Part D plan each month. If you see a charge for a doctor visit you never had or a prescription you did not pick up, it could be a sign of fraud.

Compare the dates on the MSN with your calendar or appointment records. If a service is listed for a day you were out of town or hospitalized elsewhere, flag it immediately. Keep a log of all your medical appointments, including the provider name, date, and reason for the visit. This log will help you spot discrepancies. If you find an error, contact the provider first to ask if it was a billing mistake. If they cannot explain it, call Medicare at 1-800-MEDICARE to report the suspicious charge. In many cases, Medicare will investigate and correct the record.

Choosing Trustworthy Healthcare Providers and Suppliers

Not all fraud comes from strangers: some providers or suppliers may knowingly overbill or provide unnecessary services. To reduce your risk, only use doctors, hospitals, and equipment suppliers that are enrolled in Medicare and have a good reputation. You can check a provider’s enrollment status on the Medicare.gov Physician Compare tool. Before you accept a medical device or home health service, confirm that the provider is Medicare-approved and that the service is medically necessary. If a supplier offers you something for free or says your plan covers it with no cost sharing, be skeptical. Legitimate providers will explain why the service is needed and discuss any out-of-pocket costs.

Watch for providers who waive your copayments or deductibles routinely. While occasional hardship waivers are legal, a pattern of waiving cost sharing can be a sign that a provider is billing for services you did not need. Also be wary of providers who pressure you to sign up for a service or program immediately. Take time to research the company and read online reviews. If a deal sounds too good to be true, it probably is. For further insight into larger fraud cases and their impact, you can read about Rick Scott Medicare Fraud: Unpacking the Controversy and Its Impact on Healthcare.

Using Technology and Tools to Monitor Your Account

Technology can help you stay on top of your Medicare activity. Sign up for a myMedicare.gov account to view your claims online, check your deductible status, and see your MSNs electronically. You can also set up alerts to get notified when a new claim is filed under your number. Many Medicare Advantage plans offer mobile apps that let you review your Explanation of Benefits and track your spending. These tools make it easier to spot unauthorized claims quickly.

Another useful tool is the Medicare Fraud Prevention Initiative (MFPI) hotline, which lets you report suspected fraud anonymously. You can also use the Senior Medicare Patrol (SMP) program in your state: trained volunteers help beneficiaries identify and report fraud, abuse, and errors. The SMP can review your MSN with you and offer guidance on next steps. If you suspect identity theft, consider placing a fraud alert on your credit report and notifying the Federal Trade Commission (FTC) at IdentityTheft.gov.

What to Do If You Suspect Fraud or Abuse

If you believe you have been a victim of Medicare fraud or abuse, act quickly. First, document all evidence: save emails, notes from phone calls, and copies of any bills or MSNs that look suspicious. Do not confront the suspected scammer directly, as this could escalate the situation. Instead, report the fraud to Medicare by calling 1-800-MEDICARE (TTY users: 1-877-486-2048). You can also file a complaint online through the Medicare Fraud & Abuse Reporting page on Medicare.gov.

If the fraud involves identity theft, contact the SSA at 1-800-772-1213 to report the misuse of your Social Security number. You may also want to contact your local police department and file a report. For help navigating the process, reach out to your State Health Insurance Assistance Program (SHIP), which offers free, unbiased counseling. The SHIP counselors can explain your rights and help you get your records corrected. Remember: reporting fraud protects not only you but also every taxpayer and Medicare beneficiary.

Frequently Asked Questions

What is the difference between Medicare fraud and abuse?

Fraud is intentionally deceptive: a provider bills for services never rendered, or a scammer uses your identity to receive medical care. Abuse is improper billing that may not be intentional but still wastes program funds, such as billing for a higher level of service than what was actually provided. Both are illegal and should be reported.

Can I get in trouble for reporting a false suspicion?

No. Medicare encourages reporting any suspected fraud or abuse. You are protected from retaliation as long as you report in good faith. Even if your suspicion turns out to be a billing error rather than intentional fraud, your report helps Medicare identify patterns and educate providers.

How often should I check my Medicare Summary Notice?

Check your MSN as soon as you receive it, which is typically every three months. If you have a Medicare Advantage plan, review your EOB monthly. The sooner you spot a problem, the easier it is to correct.

Are there penalties for providers who commit Medicare fraud?

Yes. Penalties can include fines, exclusion from the Medicare program, and prison time. The False Claims Act allows the government to recover three times the amount of damages plus penalties for each false claim.

Staying informed and proactive is your best defense. Review your statements, protect your card, and choose providers carefully. By taking these steps, you reduce your risk of becoming a victim. If you ever need personalized assistance, contact NewMedicare.com for guidance on your coverage options and fraud prevention resources. Call us at 833-203-6742 to speak with a licensed agent who can help you understand your plan benefits and answer questions about protecting your Medicare account.